The American financial landscape is currently navigating a quiet but significant “Post-Inflationary Credit Squeeze.” As we enter 2026, U.S. regional banks, once the lifeblood of personal and small-business lending, have significantly reduced loan originations to bolster their liquidity and manage commercial real estate exposures.

This retreat has left a staggering $3.2 billion market gap in underserved credit demand (S&P Global Ratings). For entrepreneurs, this is a massive opportunity to build the next generation of financial connectivity through a P2P lending app.

While the “Web 1.0” era of peer-to-peer lending was defined by the early success of platforms like LendingClub and Prosper, the 2026 market demands a radical technical evolution. Today’s users aren’t looking for slow, desktop-based matching; they expect a mobile-first experience powered by AI-driven underwriting that analyzes real-time cash flow and DeFi-integrated protocols.

This guide is designed as your specialized technical roadmap to navigate this high-stakes industry. We are moving beyond the basics to dive deep into the essentials, from understanding SEC registration tiers and FinCEN anti-money laundering compliance to architecting the low-latency payment rails required for a modern peer-to-peer lending application.

If you want to build a P2P payment app that leads the U.S. market, you are in the right place. All you need to do is keep sliding down.

Key Takeaways

- Market timing favors digital lenders. Traditional credit channels are tightening, and borrowers are actively looking for faster, transparent alternatives. Platforms that move early can secure supply, partnerships, and brand trust.

- Underwriting intelligence determines profitability. Combining bureau signals with real-time financial data helps approve more qualified borrowers while reducing future defaults.

- Infrastructure readiness unlocks capital. Alignment with regulators such as the U.S. Securities and Exchange Commission and the Financial Crimes Enforcement Network builds the credibility institutional investors require.

- Revenue must extend beyond interest. Sustainable platforms layer origination, servicing, analytics, and protection models so margins remain healthy across economic cycles.

Table of Contents

What is a P2P Lending App?

A Peer-to-peer (P2P) lending app is one of the growing categories of fintech app development. It is a money-lending platform where the borrowers and the money lenders are equal parties, including normal people and companies. In P2P lending apps, there is no third party (loan brokers, banks) involved during the loan lending process.

Due to the zero involvement of third parties, the interest rate is also low compared to the other traditional methods of money lending.

Also, the best thing about P2P lending apps is that you don’t need to think about any maintenance of renting premises, staff fees, computers, software, etc. The P2P lending apps work for two parties: the borrower and the lender. So, whether you are a borrower looking to get money or a lender, it’s crucial to understand the work process of loan lending.

Here’s how P2P lending apps work;

For Borrowers:

- Sign Up – Register yourself on the P2P lending app by filling in your personal information, including bank details and more.

- Profile Verification – After finishing the sign-up, you need to go through profile verification to let the lenders know the risks and rewards of lending to your business.

- Loan Market – Once you finish verification, your loan will go live, and the lenders will start bidding on your loan.

- Loan Acceptance – When you get 100% funds, accept the terms and conditions after reading them properly. It’s normal for money lending apps to charge a minimal fee for transactions of loan amounts.

- Repayment – The loan repayment date will be displayed to you in a respective section after deciding the fixed amount to pay every month.

For Lenders:

- Sign Up – Like borrowers, money lenders also need to sign up on the P2P lending apps.

- Select Account – Money lenders have different accounts, such as growth, income, self-select, etc. So, you need to choose a suitable account.

- Add Funds – After selecting the account, add funds to your app, depending on the account type.

- Lending Money – Next, start bidding for the loans that are live on the application.

- Repayment – Receive monthly repayments of capital and interest from the amount lent to the borrowers. To earn more profit, you can lend money to businesses.

Considering these features during fintech app development for your business is very crucial as they are the need of the market. Without these features, your app can’t win user trust. Apart from them, you can add advanced or customized features.

From Global Trends to U.S. Dominance: P2P Lending App Market

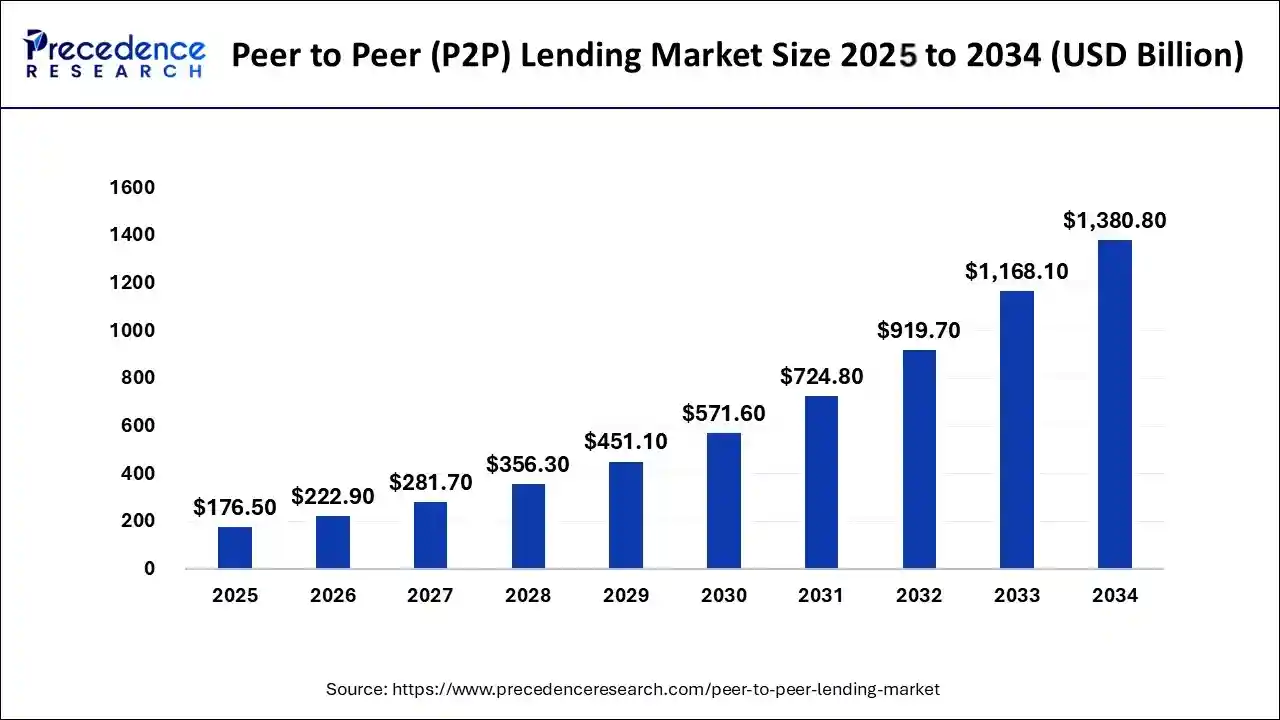

The global financial landscape is shifting rapidly. Before we dive into the specifics of the American market, it’s important to see the bigger picture. The global peer-to-peer lending app market is currently worth approximately $222.9 billion in 2026 and is projected to skyrocket to over $1.38 trillion by 2034 (Precedence Research).

This massive growth is fueled by a worldwide demand for faster, more transparent credit. However, the United States is the primary engine behind this trend, currently holding a dominant 63% share of the North American market (GlobeNewswire).

The U.S. P2P Market Stats: A Trillion Dollar Opportunity

The U.S. market is entering an era of unprecedented expansion. Analysts project that the P2P lending app sector in the U.S. will grow from $8.33 billion in 2026 to a straggering $33.8 billion by 2034, maintaining a steady CAGR of 19.1% (Fortune Business Insights).

For entrepreneurs, this means that now is the prime time to invest in P2P lending software development. The market is no longer an alternative; it is becoming a core part of the American financial ecosystem.

The Institutional Pivot: Where the Money is Coming From

One of the most significant changes in the P2P lending application space is the source of capital. We have moved far beyond the individual-to-individual model of the early 2010s.

Today, approximately 63% of North American P2P capital is supplied by Institutional Investors, including pension funds and family offices (GlobalNewswire). This institutional pivot provides your platform with the deep liquidity needed to scale quickly. By integrating Lending-as-a-Service (LaaS) architecture, you can attract these big players who are looking for stable, risk-adjusted returns.

The Behavioral Shift Towards P2P Lending Apps

Americans are flocking to P2P lending apps due to a major shift toward Debt Consolidation. As regional banks tighten their belts, U.S. consumers are using peer to peer loan apps to escape high-interest credit card debt.

By moving their balances into fixed-rate, lower-interest P2P loans, they save thousands in interest. This “Debt Recycling” is the #1 purpose for P2P lending applications in 2026, creating a steady stream of borrowers for your platform (Zion Market Research).

By understanding these market forces, you can better design your P2P payment app development strategy to meet the needs of both high-net-worth investors and the millions of Americans looking for better debt management tools.

Designing the Technical Core of Your P2P Lending App

If you want to build a successful P2P lending app, you need to think like a tech giant. In the U.S. market, users expect instant approvals and seamless fund transfers. To deliver this, your P2P lending software development strategy must focus on modular, high-speed architecture.

Instead of building every banking feature from scratch, modern entrepreneurs use a “Plug-and-Play” approach to launch faster and remain compliant.

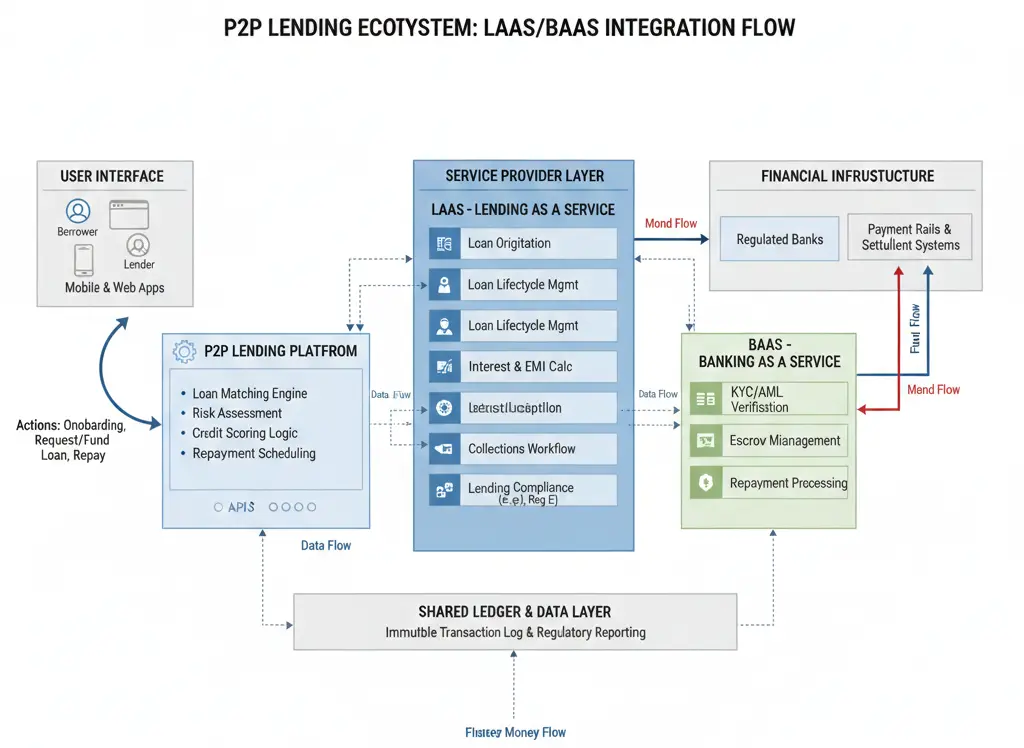

Leveraging LaaS and BaaS for Instant Infrastructure

The fastest way to build a P2P payment app is through Lending-as-a-Service (LaaS) and Banking-as-a-Service (BaaS). These models allow you to rent the heavy-duty banking infrastructure you need via APIs.

In the U.S., you should partner with established providers like:

- Unit or Bond: These platforms offer a full suite of APIs for account opening, KYC (Know Your Customer) checks, and card issuance.

- Cross River Bank: Known as the powerhouse behind many top fintech apps, their APIs handle the complex regulatory and ledgering work required for marketplace lending.

By using these services, your peer to peer lending application can focus on the user experience while the “banking” part is handled by experts in the background.

The Low-Latency Transaction Engine: Handling Real-Time Bids

A premium P2P lending app manages a live marketplace where thousands of investors might bid on a single fractionalized loan note simultaneously. To handle this without lag, your P2P payment app development team should use:

- Apache Kafka: This acts as the central nervous system, streaming massive amounts of data in real-time. It ensures that every bid and transaction is recorded and shared across your microservices instantly.

- Redis: For ultra-low latency, Redis stores data in-memory. It’s perfect for managing real-time bidding wars and pushing instant loan-funded notifications to your users.

This combination ensures that your app P2P remains stable even during peak market volatility, a critical factor in maintaining investor trust.

Choosing Your Matching Engine: Automated vs. Self-Select

How will your investors find loans? In the U.S. peer to peer lending apps market, there are two dominant models you need to consider:

Automated Investing (Algorithm-led): The app uses AI to automatically spread an investor’s money across hundreds of loans based on their risk profile. This is great for passive investors and is a standard feature for top peer to peer lending apps.

Self-Select: This gives investors full control to browse loan cards and manually pick the ones they like. It’s popular with niche investors who want to hunt for specific yields.

As a fintech app development company, we also offer a hybrid of both approaches. If you’re interested in how AI can further optimize these matching algorithms, check out our deep dive on the role of AI in fintech.

How to Develop a P2P Lending App?

To develop a peer-to-peer lending app for your fintech business, you need to learn about these money lending app development processes. These steps will help you understand how to create a money lending app. If you know these steps, you can discuss your project with any money-lending app development company freely. So, let’s dive deep into the steps one by one.

Step 1. Research the Market and Analyze Competitors

Researching the market and analyzing the competitors is crucial during money lending app development. Understand the ongoing scenario and trends in the finance sector, and research the popular P2P apps.

This research will help you understand the essential features, loopholes, and more. The more you research and analyze, the more your app will benefit from it.

Remember to write down the information that can be beneficial for you during P2P lending app development. Writing down this information will help you understand what your customers want so you can fulfill their needs.

Step 2: Don’t Forget to Adhere to Security Compliance

Security is one of the major factors while developing a P2P lending app because banks become targets of more than 30% of malware attacks. Users prefer to avoid such lending apps that don’t follow security protocols. Therefore, you need to implement the following things –

- Encryption: Strong encryption is needed for money lending apps. You need to ensure that your app includes connections from secure servers that are integrated with a data-breaching structure.

- Authentication: This process improves the security of your P2P lending app because it includes multiple identity verification approaches like Passwords, 2-factor authentication, face recognition, and fingerprint scanning.

- Legal Law Compliance: Your micro lending app needs to be legally compliant with the current rules and regulations and follow data security standards like being SOC 2 Compliant. This ensures the safety of personal data and sensitive information.

- Enterprise Security Configuration: Establishing your business under a suitable business structure, such as an LLC, with guidance from legal professionals, can add an extra layer of legal protection. It helps separate personal and business liabilities, which is crucial in the fintech space where regulatory and financial compliance are vital.

Step 3: Select the Right Business Model To Be Profitable

Every mobile app development company puts a lot of effort and time into developing a mobile app. The same process is followed while building P2P lending apps. So, you need to choose a suitable business model. It will play a huge role in making your application profitable and rewarding.

The recommended business models are advertising, subscriptions, and commission-based models to ensure continuous income from your peer-to-peer lending app.

So, you must ask the mobile app development company to choose a business model specialized to your business needs and demands. It will have a huge impact on the success of your application.

Step 4: Choose Necessary Features to Stand Out

Features are important parts of every application and website. They can decide the success or failure of your business. So, you must add the right set of features to your lending online app. But don’t exceed your budget after being attracted by advanced features. AI and machine learning are changing the money lending landscape. So, remember to use them in your online app.

If you have a huge budget for your P2P lending app, then you can choose advanced features for your lending app. They can make your app unique and add value to your business. Here are some features you can include in your micro lending app;

- User Registration and Profile: Users should be able to sign up easily using their email, phone number, or social media accounts. A separate profile for lenders and borrowers should be included, with options to switch roles.

- Loan Application Process: Borrowers should be able to select the loan amount, terms, and repayment period. Also, it allows borrowers to upload required documents.

- Loan Listings and Lender Search: Allow borrowers to list their loan requests with terms and interest rates. Lenders can browse through loan requests and filter based on rates, duration, or borrower risk profile.

- Investment Dashboard: Lenders should be able to track their investments, returns, and risk exposure. They can choose to invest in multiple loans to diversify the risk.

- Loan Calculator: A loan calculator helps borrowers to calculate their installments and the total amount as well by entering tenure, loan amount, and interest.

- Payment Gateway Integration: A seamless gateway allows smooth deposits and withdrawals.

- Notifications: Notifications for loan approval, investment confirmation, and repayment dates. Along with this, sending alerts on any changes is crucial.

- In-App Camera & Chat: Allows users to upload images of documents, while call & chat features connect lenders to borrowers.

- Chatbot Support: Provide 24/7 support services to your users so that they don’t switch to the app in case of support.

- Loan Management: This feature will allow you to keep all records of the loan, amount, transactions, histories, lender, and borrower details.

Step 5: Choose Appealing UI/UX Design to Grab User’s Attention

Consider including an appealing design that can grab users’ attention at first glance. Users can choose your peer to peer lending app if it has an attractive design. But make sure to make your business app easy to navigate.

Look for an experienced UI/UX design agency to include an appealing design in your application. But don’t forget to check whether they have talented designers on their team. Also, remember that modern technologies will ensure the success of your P2P lending app in the coming time.

Step 6: Create an MVP To Save Money

Creating an MVP (Minimum Viable Product) is the best way to validate the idea of your micro lending app. Choosing MVP development will save you time and effort in creating peer to peer lending app. It will also help you eliminate errors and bugs before the official launch of your application.

Also, MVP can save P2P lending app development costs and help you save your valuable money. So, before going for final application development, create an MVP to pave the path for the success of your vision.

Read Also : Real-Life Examples of Successful MVP Development For Startups

Step 7: Develop and Test Your Peer to Peer Lending App

Last but not least, develop a micro lending app by following all the steps mentioned above. When you build a P2P lending app successfully, it’s time to test your application using the latest tools to make it 100% error-free. If you launch an app with errors, no user will use your app. So, it’s crucial to follow all the steps while building your application.

These steps are necessary to develop successful and revenue-generating P2P lending apps. Now that you are well-versed in the development process, let’s know how much it costs to build P2P lending apps.

Automated Risk Management to Safeguard Revenue

In the U.S. lending market, managing risk is the difference between a thriving platform and a failed venture. To maintain users’ trust, your P2P lending app must go beyond the traditional FICO score. Top platforms use a hybrid model of traditional credit data and real-time behavioral insights to ensure a zero-default strategy.

Beyond FICO: Alternative Credit Data (ACD)

The traditional credit score often ignores millions of thin-filed borrowers who are actually creditworthy. To capture this market, your P2P lending software development must integrate Alternative Credit Data (ACD).

- Use APIs like Plaid or Finicity to analyze a borrower’s income and spending habits directly from their bank accounts.

- Mention integrating with services like Experian Boost. This allows users to add positive payment history from utility bills and streaming services directly to their profiles.

By using ACD, you can approve more borrowers with lower risk, which is a major selling point for investors on your P2P lending app.

NPL Management AI: Predicting Defaults Before They Happen

A non-performing loan (NPL) is a nightmare for any P2P lending app. In 2026, the gold standard is using an AI-driven NPL management module.

- Instead of waiting for a missed payment, this AI analyzes “spending pattern shifts.” For example, if a borrower suddenly stops their regular gym membership or starts spending more at discount grocers, the AI flags a potential liquidity issue.

- Once flagged, the app can automatically offer a “hardship pause” or a restructured payment plan. This human-centric AI approach can reduce defaults by up to 15-20% (Industry Report).

Navigating U.S. Legal & Compliance Requirements

Compliance is not just a hurdle; it is your competitive advantage. For a P2P lending app in the U.S., trust is built on a foundation of strict federal and state oversight.

Securities Compliance

How you raise money and offer loans to investors depends on SEC regulations.

- Regulation D (Private Placements): This is the fastest way to start. It allows you to raise unlimited capital from “Accredited Investors” with fewer reporting requirements.

- Regulation A+ (The Mini-IPO): If you want to allow everyday retail investors (non-accredited) to fund loans, you need Reg A+. It allows you to raise up to $75 million annually but requires more extensive SEC disclosures.

Federal Oversight: FinCEN and CFPB

Your P2P payment app development must bake compliance into the code:

- FinCEN (AML/BSA): You must implement Anti-Money Laundering (AML) protocols to report suspicious activity and verify user identities (KYC).

- CFPB (Fair Lending): The Consumer Financial Bureau ensures you aren’t using biased AI algorithms. Your AI credit scoring must be explainable to prove it doesn’t discriminate based on protected classes.

State-Level Licensing vs Bank Partnerships

In the U.S., lending is regulated state-by-state. You have two choices:

- Direct State Licensing: You apply for a Money Transmitter or Lending License in all 50 states. This is expensive and slow.

- The Bank Partnership Model: Partner with an FDIC-insured bank. By doing this, you can lend under their federal charter, effectively bypassing individual state caps and launching nationwide much faster (Payments Dive).

Data Sovereignty: PCI-DSS and SOC2

- PCI-DSS Level 1: If your app handles card payments, this is mandatory. It ensures your P2P payment app development meets the highest security standards for transaction data.

- SOC Type II: This proves to your institutional investors that you have long-term, audited controls over data privacy and system availability.

The Tech Stack For Building a P2P Lending App

To maintain a low-latency trading architecture, your tech stack must be modern, scalable, and secure. Ensure your fintech app development services provider uses this tech stack to achieve better results.

- Frontend (The User Experience): Flutter is perfect for high-fidelity consumer apps. It allows you to maintain a single codebase for iOS and Android while offering near-native performance.

- Backend (The Logic Engine): Use Node.js for high-concurrency tasks like real-time bidding and notifications. Python is also the industry standard for building an AI-driven underwriting engine due to its rich library of machine learning tools.

- Database (The Vault): Use PostgreSQL for transactional integrity. Every loan and payment must be recorded with 100% accuracy. For global scaling, Amazon Aurora allows your P2P lending app to handle massive growth across different U.S. regions without downtime.

How Much Does P2P Lending App Development Cost?

The average P2P lending app development cost ranges from $25,000 to $90,000, depending on the type of mobile app. However, several factors will affect the cost of development. You can use our App Cost Calculator to understand the final cost. Explore the latest estimates below:

| Development Phase | MVP (The Lean Startup) | Full-Scale (Business-Ready) | Enterprise (Market Leader) |

| Estimated Cost | $150,000 – $250,000 | $450,000 – $750,000 | $1M – $2.5M+ |

| Timeline | 3–5 Months | 7–10 Months | 12+ Months |

| Core Focus | Plaid integration, KYC, and basic matching. | AI underwriting, automated debt recovery. | Multi-region scaling, DeFi pools, and advanced NPL AI. |

The Hidden Pillars of Fintech App Development Costs

To avoid budget overruns, you must partner with an experienced mobile app development company in USA. But before that, we are here to provide the hidden factors that impact the cost of a P2P lending app:

- Legal & SEC Filings ($40k – $80k): Preparing Regulation A+ or Regulation D filings with specialized U.S. fintech attorneys is mandatory.

- Security Audits ($20k – $40k): SOC Type II and PCI-DSS Level 1 certifications are essential for gaining the trust of institutional lenders.

- BaaS/LaaS Integration Fees ($5k – $15k/month): While APIs like Unit or Cross River Bank save you millions in infrastructure, they carry monthly platform fees and per-user transaction costs.

- Annual Maintenance: Budget 15-20% of your initial build cost annually for security patches, cloud hosting (AWS/Azure), and feature updates.

Monetization Strategies For Your P2P Lending App

Building a P2P lending app that wins user trust isn’t just about having the best tech; it’s about having the most resilient business model. In 206, top platforms like Upstart and Prosper have moved beyond simple interest to a diversified Revenue Stack.

Primary Revenue Streams

Origination Fees (Borrower-Side): This is your bread and butter. Platforms typically charge a one-time fee of 1% to 8% of the total loan amount, deducted immediately upon disbursement (Equifax).

Servicing Fees (Lender-Side): You charge investors a small monthly fee (usually 1% annually) for managing the loan, collecting payments, and providing tax documentation.

The Spread (Premium Model): Some platforms keep a portion of the interest rate. If a borrower pays 12%, the investor might receive 11%, while the app keeps the 1% spread as a platform fee.

Advanced & Next-Gen Monetization (New Trends)

- DeFi Liquidity Pools: By integrating DeFi Lending Protocols, your app can act as a gateway for stablecoin (USDC) lending, taking a gas fee or convenience fee for bridging traditional and decentralized finance.

- Premium Data Subscription: Charge institutional investors for Deep-Dive Analytics, which are AI-generated reports that provide a granular look at borrower behaviors and market risk trends.

- Late Fees & ADR Recovery: While we aim for a zero-default strategy, when defaults happen, the app earns a precentage of the recovered funds through Automated Debt Recovery (ADR) modules.

- Embedded Insurance: Partner with InsurTech to provide Loan Protection Insurance. If a borrower loses their job, the insurance covers the EMI, and you take a referral commission.

By diversifying your income, your P2P lending app remains profitable even during periods of low interest rates or economic volatility.

Final Words

We hope this blog has helped you understand how to create a successful P2P lending app in 2026. Nevertheless, developing a P2P lending app is quite difficult. It requires time, effort, and expertise to help businesses earn huge and build a strong foothold in the finance sector. But now that you have an idea of everything, you need to begin the process properly. However, you must partner with a custom app development company.

RipenApps, a leading company experienced in developing advanced P2P lending apps, can be your reliable partner. We have a certified team of developers and helped businesses achieve their business goals with smart apps. In the fintech market, we have helped businesses achieve remarkable results. Apps like Al Muzaini and Cotax did the best in their segment and left the competition behind, achieving the best results.

So, when you partner with RipenApps, you get an experienced partner that can transition your vision into reliable & top-performing applications. Having the experience of nearly a decade, our experts have deep knowledge of the fintech market and they help you maximize your ROI.

FAQ’s

Q1. What is the Average Cost to Develop a P2P Lending App?

The average cost of developing a P2P lending app ranges between $25,000 to $90,000. However, the cost can fluctuate based on different factors that are necessary to consider while developing your dream app.

Q2. What are the Top P2P Lending Mobile Applications?

The top P2P lending mobile applications are Prosper, Lending Club, Peerform, Upstart, and Payoff. These apps have gained popularity after providing seamless services.

Q3. Can I Start a Peer-To-Peer Lending Business After Creating an App?

Absolutely, you can start your P2P lending business after developing an app. You should remember some steps like; regulation, security, credit risk assessment, and privacy.

Q4. How do P2P Apps Make Money?

P2P lending apps make money by charging fees for their services. Apart from that, mobile app monetization is also crucial to making money with P2P lending apps.

SHARE

WRITTEN BY

Prankur Haldiya

Chief Technical Officer

A tech innovator and engineering leader, Prankur Haldiya drives RipenApps’ product development strategy and oversees cutting-edge solutions in mobility, AI, and cloud ecosystems. He is passionate about building high-performance teams and helping brands launch secure, scalable, and user-centric digital products.

View All Articles